Part 1: The Offshore Connection

I was a bit perplexed with all the hoopla over the Adanis in the recent weeks. In this blogpost I hope to cover a few key themes on concerns about the company in the media.

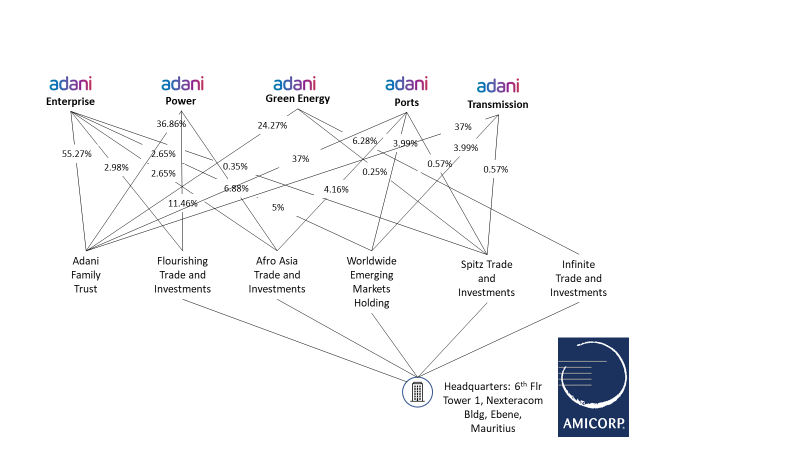

Firstly, does Adani have any offshore connection. There is absolutely no mystery to me. They have direct offshore links in all of their public listed companies except Adani Wilmar and Adani Total Gas Ltd. This diagram should put it to rest and hopefully simplify the picture.

Adani listed companies are predominantly owned by Adani Family Trust, family trusts are opaque structures, and we don’t know who sits behind them. If we look beyond the trust the majority shareholders are offshore companies located in Mauritius. All of them own below 10% shares in each of the companies, which keeps them below the unwrapping requirements. When you add the shareholding across all the offshore entities the ownership can be as high as 18.38% for a company as in the case of Adani Power. Banking regulations mandate that they verify the identity of their client’s owners up to 10% shareholding, this is called unwrapping. So this would mean, these offshore companies can operate under the regulatory scanner. One will have to speculate here, if indeed these offshore companies are meant to hide Adani’s as the ultimate beneficiaries, adding these offshore company’s to the Adani family’s ownership would increase in some cases the family’s total holdings to beyond the 75% maximum promoter holding.

Next, all of these offshore companies are listed in the GLEIF or Global Legal Entity Identifier. GLEIF is the global company information database and interestingly all of the Mauritius investors are registered and headquartered at 6th Floor Tower 1, Nexteracom Bldg, Ebene, Mauritius.

Now why would all these investment companies have the same address and the same floor even (6th floor) as Amicorp Mauritius Ltd? It’s very common for a company secretary to list their office address as the registered address on behalf of a company until the it takes off. I have done so for large corporations when entering a new market. This also helps the company secretary deal with all company and legal affairs initially. But for companies registered since 2015 to have their headquarters (not only registered address) listed as that of their company secretary’s is very unusual. So it is quite likely that these companies have no physical presence and they are using Amicorp Mauritius Ltd as their physical presence. It’s very common for shell companies that mean to obfuscate the underlying investors behind them to operate this way.

What is also worth noting is none of Adani’s offshore investment companies have parent or child companies listed. This further increases the likelihood of them being shell companies. But at the least they are opaque structures just beyond the regulatory reach

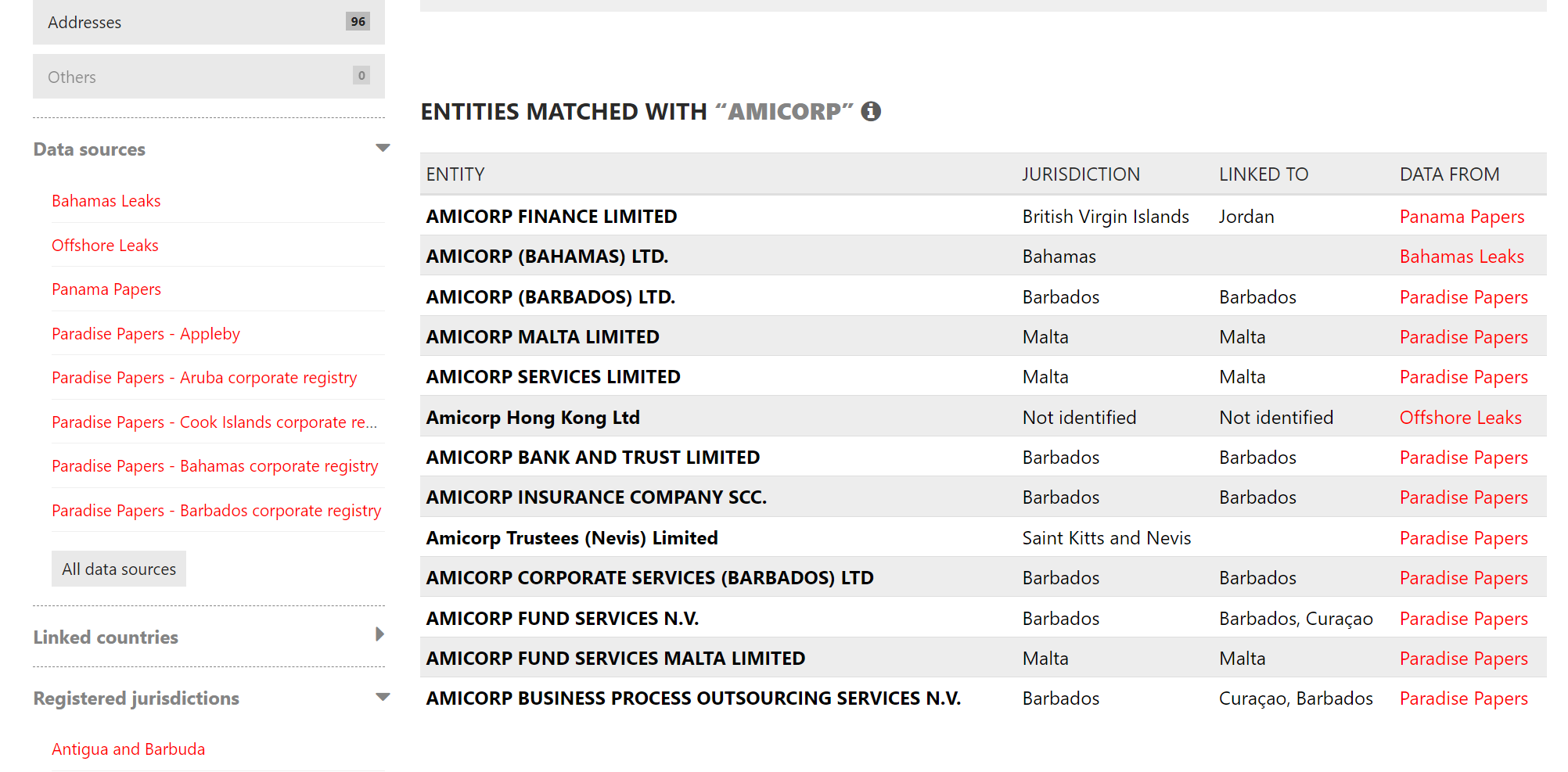

I looked into Amicorp in ICIJ’s (International Consortium of Investigative Journalism) database that has decoded the millions of offshore entities listed in the Panama papers and the Paradise papers amongst others. And lo and behold look below:

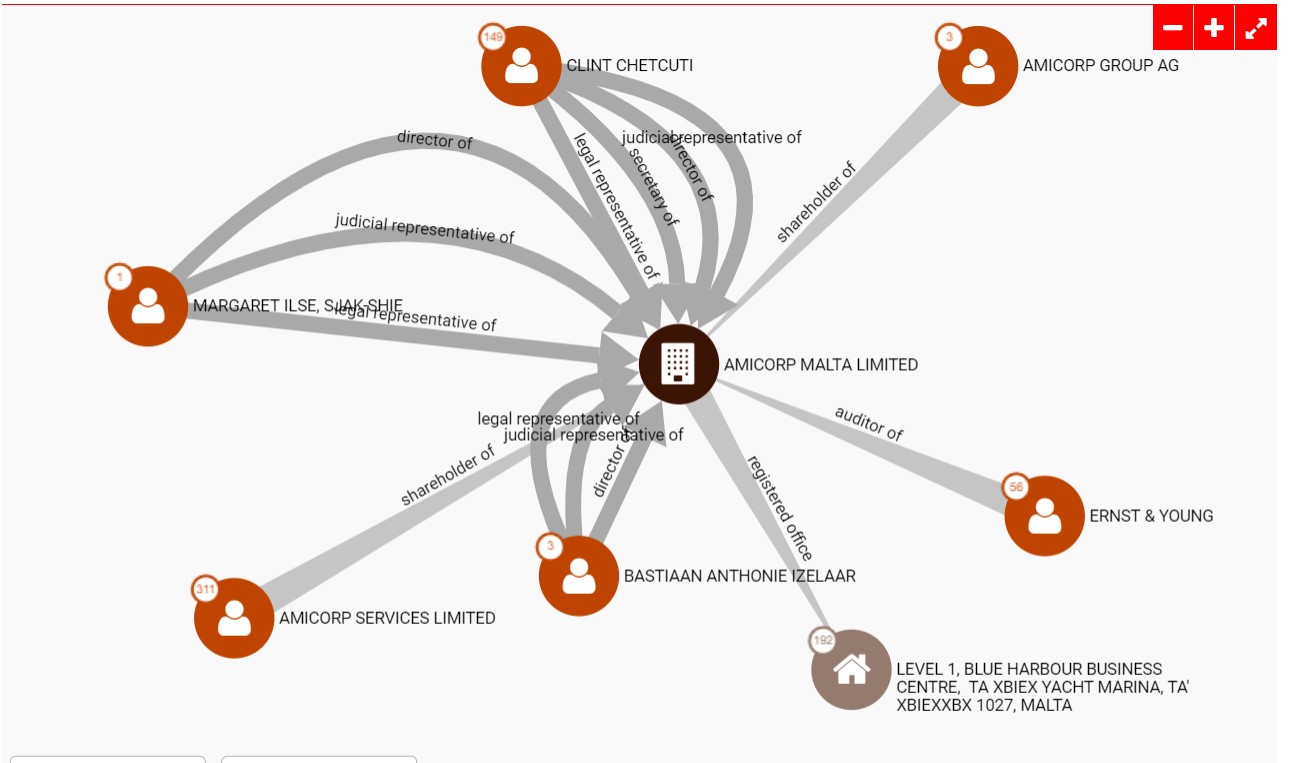

What is important to note is that a company’s name, if merely listed in Paradise papers does not make it bad. Amicorp Services Ltd and Clint Chetcuti, a director in Amicorp for 7 1/2 years, have association to 311 and 149 companies listed respectively in the Panama/Paradise papers respectively, surely that has to be a matter of concern.

If that doesn’t raise concerns, Amicorp’s involvement with 1MDB should, they have been instrumental in facilitating pilfering of $5.6 millions for Mr Yeo an ex 1MDB banker who was found guilty and sentenced to 30 months in prison by Singapore courts. What was damming in Yeo’s sentencing is when he instructed Amicorp’s relation manager to destroy critical evidence to the 1MDB case.

Amicor bank also has outstanding litigation for laundering $100s of million via Amicorp bank in the 1MDB case in U.S. courts. So the question is why would a company of Adani’s stature use the services of a firm with Amicorp’s suspicious reputation? One can only hazard a guess but definitely warrants a thorough investigation by the regulator as there in enough gun powder here to trigger regulatory red flags.

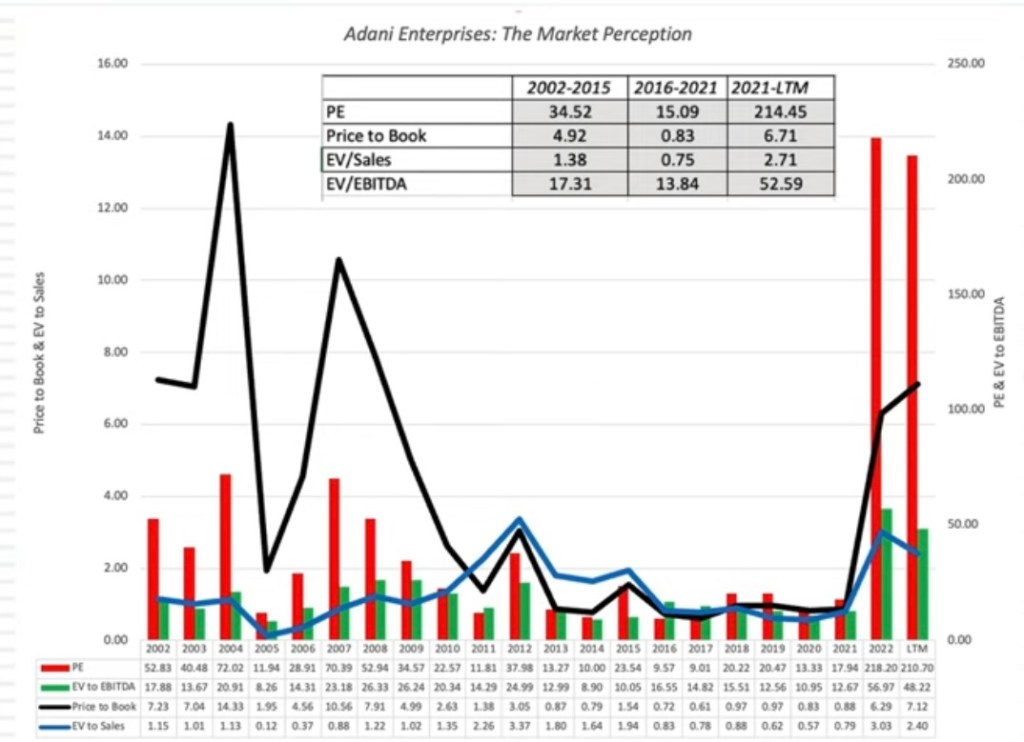

The above chart is from a valuation video by the valuation expert professor Ashwath Damodaran, which I have linked to and definitely recommend one must watch. But looking at the charts what stands out (a gross understatement) is the PE rise from 17.94 to 218.20 in a year with no significant change to the underlying fundamentals of the company to warrant such an astronomical rise. This should give reason for the regulator to look into the deals during the period especially if it’s block deals emerging from Mauritius investors.

Let’s now look at Adani’s appetite for borrowing. Adani is a heavily leveraged firm with significant reliance on debt, but let’s look at the facts first. Adani Enterprises had a net debt-to-ebitda ratio of 10 times as of the financial year ended March 2022, according to calculations by Fitch company CreditSights, one of the highest in the conglomerate. But it requires further spending to meet its targets, with plans to more than double annual capital expenditure to Rs400bn ($4.88bn) both this year and next. Adani Green Energy has a debt / equity ratio of 20:1 times, which makes Adani Green Energy the second most leveraged company in Asia.

So a company with such high debt to equity ratio stands to gain if their equity value appreciates significantly vis a vis their debt. They would also stand to gain even more if they were to raise capital via an FPO at such a premium. Raising capital will also lower their already very high cost of capital. Also if indeed their borrowings is against their shares then it enables them to borrow some more to meet their ambitious growth plans. Finally given the low margins of between 3-4% and such high debt to equity ratio it becomes harder to justify such high equity multipliers. All of this warrants RBI to take a hard look at Adani’s credit portfolio to closely examine its impact on the banks with significant exposure to the conglomerate.

Finally it’s disappointing to see the lack of any regulatory intervention, when the Adani stock has been spiralling downwards and the media has been rife with speculation. Surely a responsible regulator will put forth the facts to quell all the wild speculation? Or have the regulators been sleeping at the wheel and have they been caught napping? I am hoping we would not have to wait too long for the answers.

1 Comment